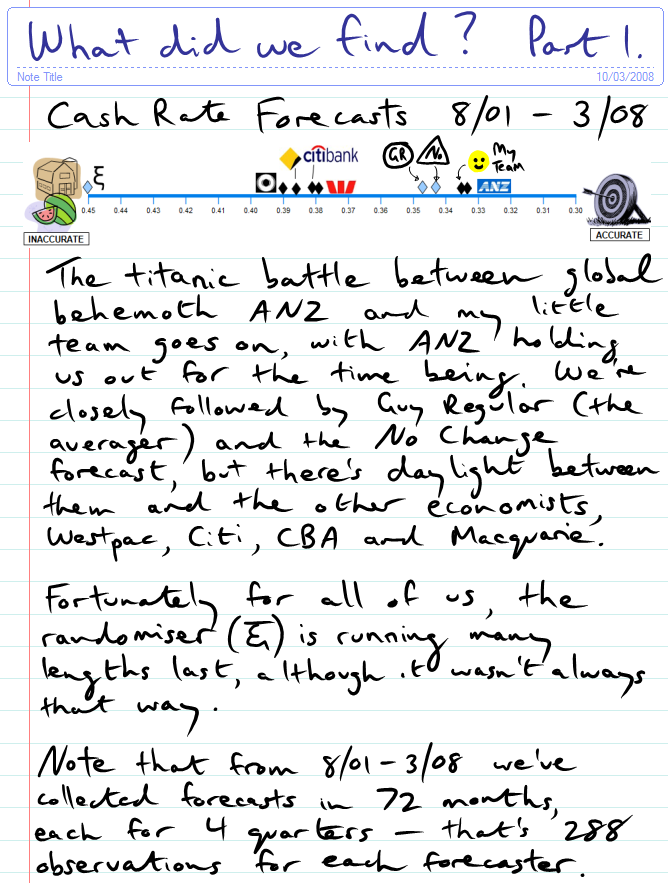

What are we measuring? We're measuring the forecasting accuracy of a bunch of economists here in Australia. As you'd know, these people are flat out forecasting everything under the sun, pausing to rest only on the Sabbath and (presumably) bank holidays. Amongst the plethora of indicators available to us, one stands out as a clear benchmark: the Reserve Bank's official cash rate. This rate, like the Fed Funds rate in the US, is so central to everything that goes on in the financial markets that it's absolutely critical that you get it right. Or so you'd think. Anyway, cash rate forecasts are readily available, and are updated regularly. So, at the start of every month* we get the economists' forecasts for the cash rate for the next 4 quarters. *except January _ taking the RBA's lead (they don't meet January) we just ignore this month.

[+/-] Hide/Show Text

[+/-] Hide/Show Text